Chapter 16 — The Future

“The more things change, the more they stay the same.”

— A proverb loosely translated from “plus ça change, plus c’est la même chose”

When asked what he thought the stock market would do next, J.P. Morgan answered,

“It will fluctuate.”

The global Internet Peering Ecosystem continues to evolve and morph to meet the demands of its users and their applications. Over the past few decades we have seen the peering model evolve from network-based metro-area peering to carrier-neutral IXP-based peering. In 2014 we will see more Remote Peering interconnection blended with Internet Transit, Traditional Peering, CDN, and full-POP deployments.

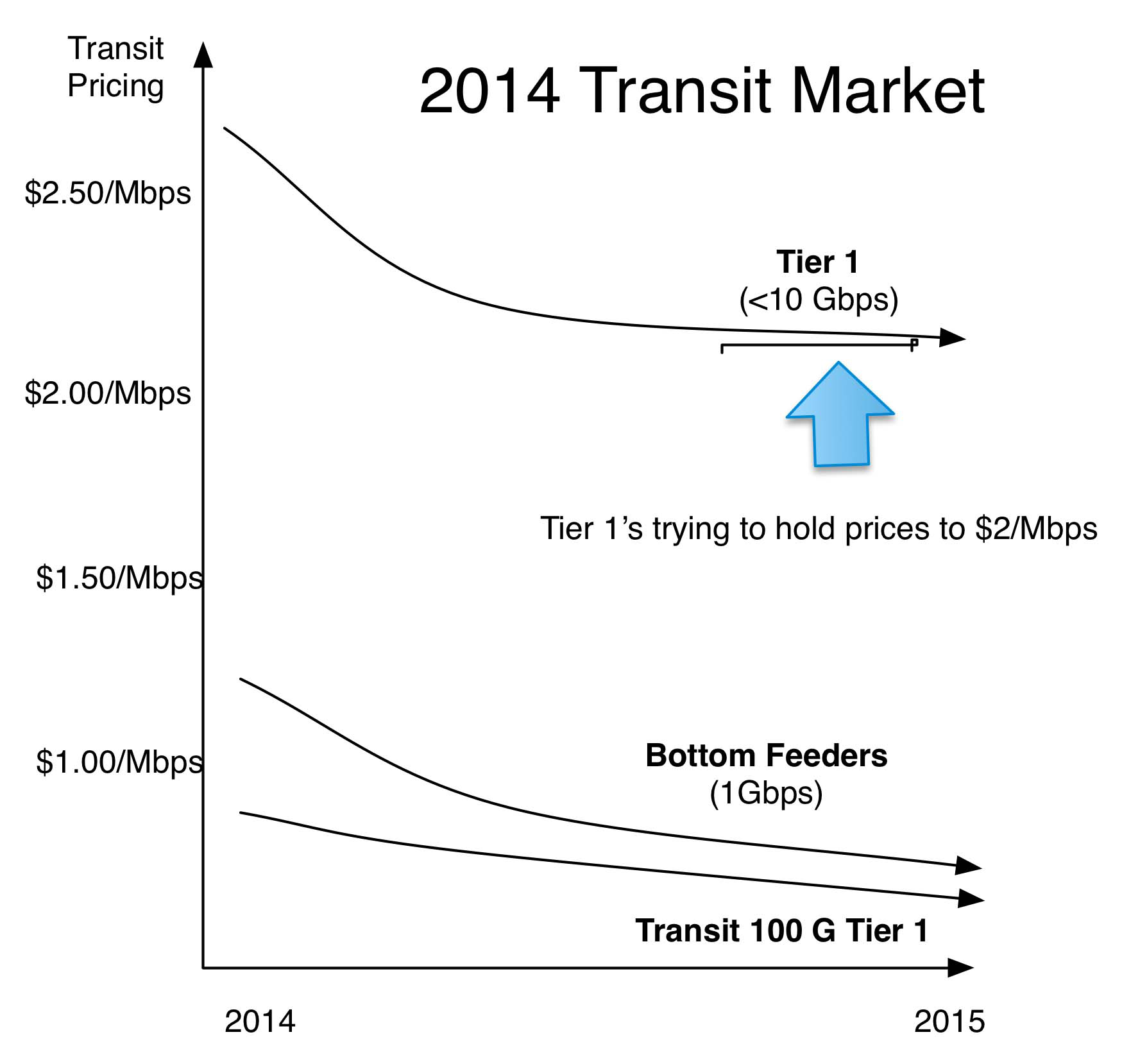

Internet Transit in 2014

The Tier 1 ISPs in mature Internet Peering Ecosystems will try to hold their ground on price in 2014. As in 2013, we will continue to see this as a bifurcated Tier 1 pricing model across commit levels. For example, Content Providers with less than 10Gbps will continue to have a hard time getting below $2/Mbps from Tier 1 ISPs such as Level 3. Only when buying more than 10G will customers see pricing towards the $1/Mbps price range from the Tier 1’s.

Of course, at the extreme end of the scale, those buying on the scale of Apple, Facebook, Microsoft, Netflix etc., in the 100Gbps+ range, will see $0.40/Mbps price points throughout 2014 from the Tier 1 ISPs. These same content providers will have no problem though getting a 1G service for less than a dollar from the bottom feeders. Taken together, these trends are described in Figure 16-1.

Across the board in 2014, Internet Transit prices will be very inexpensive, but there will be markets of exception. For example, I gave a talk for the US Telecom folks in Lake Tahoe a few years back when a rural Texan ISP approached me and said “We don’t see prices anywhere that low — we pay $75/Mbps because there is only AT&T there.” Less mature peering ecosystems like these will see outlier prices as high as hundreds of dollars per Mbps. The good news for these folks is,

“the bottom feeders are coming to town in 2014.”

Internet Peering in 2014

Peering between ISPs in the U.S. and across Western Europe is pretty much done, in the sense that most ISPs that need to peer with each other are already doing so. Major Internet Peering Ecosystems across Asia, such as Japan, Hong Kong, etc. and parts of Eastern Europe and Russia, are also mature peering ecosystems, as evidenced by low Internet Transit prices.

There are many aspects to the value proposition provided by Internet Peering. Peering makes sense financially if enough traffic can be exchanged to cover the costs of peering. Peering makes sense logistically when the value derived from peering, including the performance benefits, the security benefits, along with the operations benefits, collectively exceed the cost of peering.

Let’s look at some of the things that will drive these peering values into 2014.

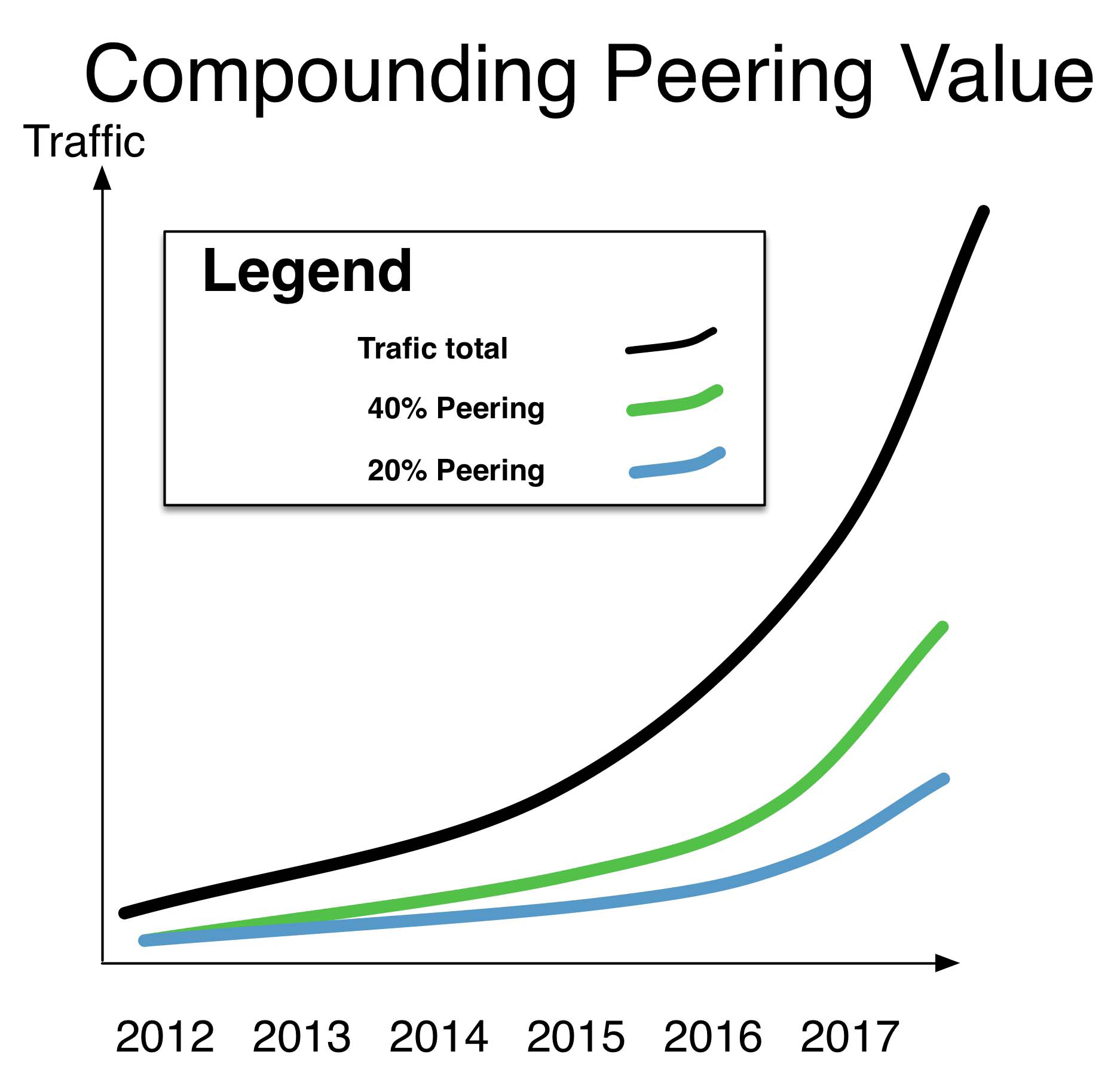

1) Internet Traffic Always Grows, so the Value of Peering Always Grows

Internet traffic has always grown and will continue to grow through 2014. As the amount of Internet traffic grows, the amount of traffic one can peer away for free grows, and so the benefits of peering will continue to grow as well.

Even more, the value of peering tends to get compounded since peering coordinators continually add peers over time. For example, most network operators in the first few years will grow their peering 30%–50% to peering as shown in Figure 16-2. The benefits of peering will compound since the peered traffic grows at a faster rate over time as more peers are added. This compounding makes the value of the major market IXPs grow exponentially.

But with transit prices so low, won’t rational peers pull out of IXPs?

It depends.

- Some will still be able to peer away enough traffic to completely cover the cost of peering.

- Some will peer no matter what, purely for performance or security reasons.

- Some will continue to peer, even when it is more expensive to do so, because they don’t want to signal to the market that they are in a decline or running out of money.

- Some will keep peering because they don’t realize that peering is more expensive than transit; they simply don’t do the math.

And some will pull out of peering and resell someone else’s network. Those that go this route better have a strong differentiator, because otherwise they will have repositioned themselves as a commodity Internet reseller and ride the price curve down towards zero.

In sum, the Internet growth curve will drive the peering market segment growth and therefore the peering value proposition.

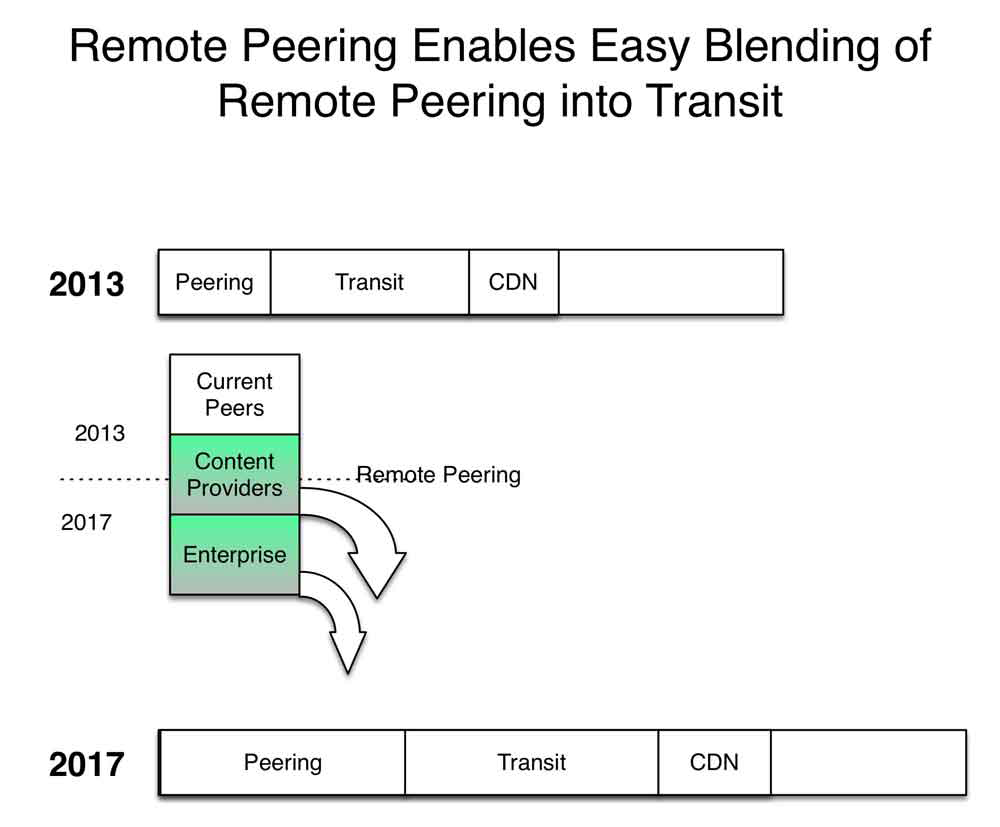

2) Remote Peering Grows the Peering Market

Remote Peering enables large enterprises, content providers, e-commerce and portals, to start peering without having to be a network operator. Without the cost of routers, colocation space, and a large network team, these companies will be able to directly connect their content to the core of the Internet. This leads to more peers, more traffic, and therefore a greater peering value proposition for peering. Because of Remote Peering, the proportion of content providers and enterprises peering at the exchanges will grow in 2014.

Network-savvy enterprises will internally justify peering for the security benefits of peering, the control over routing, and bypassing the commodity Internet for direct access to their customers and service partners. In addition, small Content Providers and Cloud Services Providers in particular will start remote peering with relevant niche trading partners to help them scale. Once peering is seen as obtainable and strategic, these new peering participants will bring new traffic and new routes to the peering points over the next few years as shown in Figure 16-3.

3) Emerging Ecosystem Regional Growth Drives Traffic to Mature IXPs

Peering ecosystems across Africa and elsewhere will continue to extend their network reach into mature ecosystems to obtain inexpensive transit. While this may slow the development of local content and therefore the rate of local ecosystem growth, it will drive the value of peering at the mature IXPs. These new routes and resulting increased traffic volume will result in lower prices back in the local market with better performance. The traffic growth in these other regions will lead to a stronger peering value propositions at the mature IXPs.

In 2014, expect to see many more customers connecting to the large European IXPs and the emerging regional IXPs on other continents as well.

4) Video and New Traffic Types will lead to Distributed Peering Load

Video and new types of traffic will drive Internet traffic volume. Video is already 50% of all Internet traffic, and I believe the video ecosystem will require wider distribution across many more peering points, perhaps helping to establish the viability for many more IXPs across the Tier 2 and Tier 3 cities. Within a few years, these new IXPs will exchange as much traffic as the larger U.S. IXPs in Tier 1 markets today shown in Figure 16-5.

The distribution of IXPs into the Tier 2 and Tier 3 cities will make it less expensive for the new peers to start peering and thus drive peering growth.

5) New Power Requirements Drive Distributed Peering Growth

Compounding this distribution effect, power requirements for dense server deployments will also lead to peering growth. There will be a new Request For Proposal put out for the next generation Tier 1 ISP interconnect points, backed by the large-scale cable companies, video distributors and partners, and large-scale content companies. They will deploy dense server clusters across this much more widely distributed ecosystem of IXPs.

Between 2014 and 2017 expect to see the eight interconnection regions where the Tier 1 ISPs peer, evolve to perhaps 80 IXPs across North America, each supporting massive clusters of Netflix and YouTube videos along with whatever else the Internet consists of. Given that these two content providers represent 50%+ of the Internet traffic, Google and Netflix have the clout to drive the market towards making these 80 IXPs the must-peer locations. There are other initiatives in the workings as well relating to data centers in the last mile and massive centers near the legacy IXPs. The Tier 1 ISPs might originate this RFP, but the content companies will demonstrate the power to drive fundamental changes to the peering ecosystem.

∗∗∗ ˜˜˜ ∗∗∗

Predictions, graded

An AI pass over this chapter against 2026 reality.

Transit prices keep falling, measured in cents/Mbps

ConfirmedVideo reaches ~80% of Internet traffic

ConfirmedInternet morphs into a video-distribution supply chain

ConfirmedNext-gen IXP racks will need ~20 kVA

Wrong magnitudeTier 1s lead the move to new facilities via RFP

Partial · hyperscalers leadEastern Europe / MENA / Africa grow dominant regional IXPs

ConfirmedInternet stays glued by transit + peering

ConfirmedAnnotations and grading generated by an LLM with the full book and current peering data sources as grounding. Toggle off with the ✦ button in the header.

The Future of the Internet Peering Ecosystem

The Internet Peering Ecosystem will evolve, but fundamentally will remain glued together with Internet Transit and Internet Peering relationships.